On the Eve of a Significant Dollar Devaluation, Bitcoin is Poised for the Final Spark

Original Article Title: BTC: Onchain Data Update + our views on last week's FOMC and the "big picture"

Original Article Author: Michael Nadeau, The DeFi Report

Original Article Translation: Bitpush News

Last week, the Federal Reserve cut interest rates to a target range of 3.50%–3.75%—this move was fully absorbed by the market and largely expected.

What truly surprised the market was the Federal Reserve's announcement to purchase $400 billion in short-term Treasury bills on a monthly basis, which quickly earned the label of "QE-lite" by some.

In today's report, we will delve into what this policy change really means, what it doesn't change, and why this distinction is crucial for risk assets.

Let's get started.

1. "Short-term" Outlook

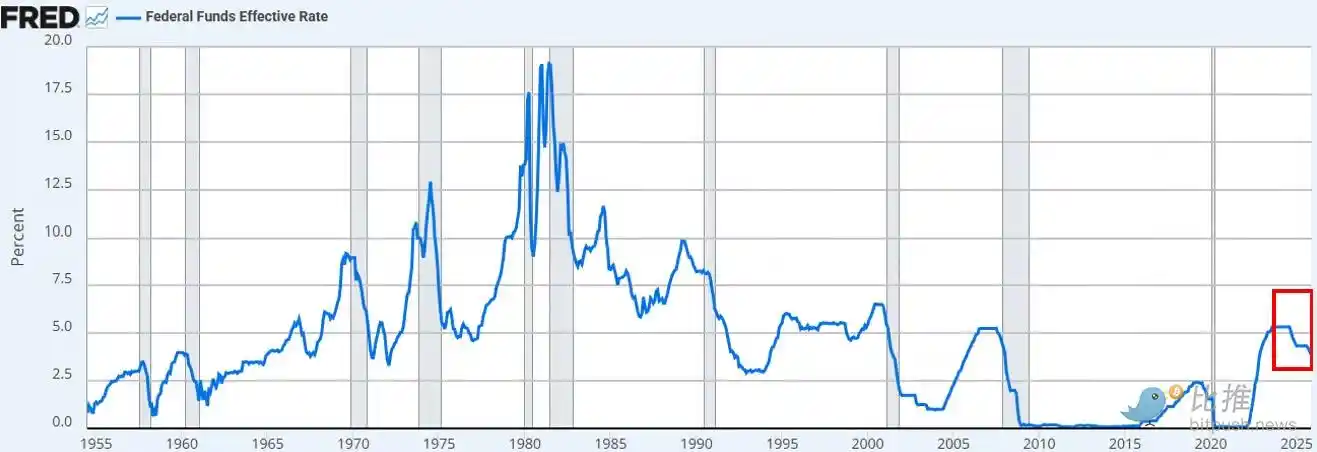

The Federal Reserve cut rates as expected. This is the third rate cut this year and the sixth since September 2024, totaling a 175 basis point reduction and pushing the federal funds rate to its lowest level in about three years.

In addition to the rate cut, Powell announced that the Fed will begin "reserve management purchases" of short-term Treasury bills at a pace of $400 billion per month starting in December. Given the ongoing strains in the repo market and bank sector liquidity, this move was entirely within our expectations.

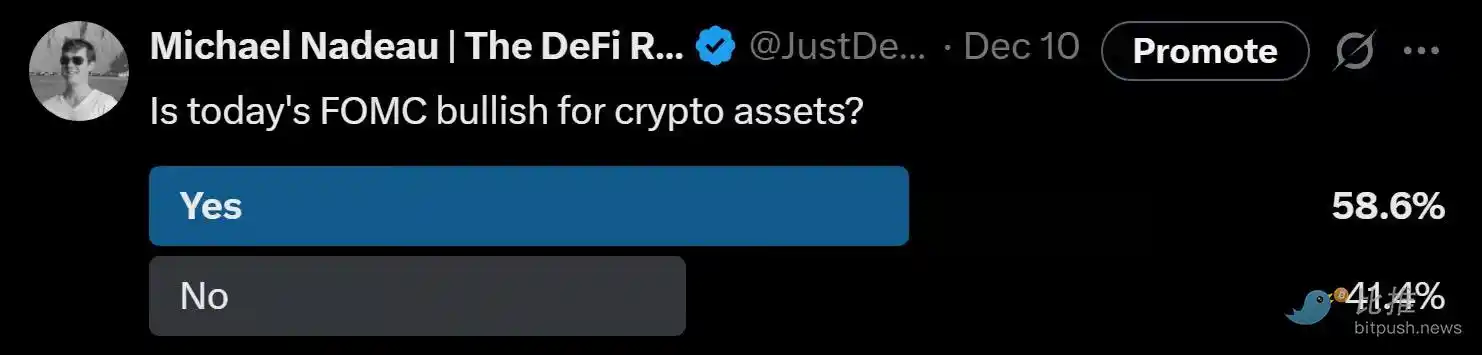

The prevailing market view (whether on X platform or CNBC) is that this is a "dovish" policy shift.

The debate on whether the Fed's announcement is equivalent to "money printing," "QE," or "QE-lite" immediately took over social media timelines.

Our Observation:

As a "market observer," we find that the market's psychological state still tends towards "Risk-on" sentiment. In this state, we expect investors to overly fit policy headlines, trying to piece together a bullish logic while overlooking the specific mechanism of how policy translates into actual financial conditions.

Our view is: The Fed's new policy is favorable for the "financial market plumbing," but not favorable for risk assets.

Where do we differ from the market's general perception?

Our views are as follows:

· Short-Term Treasury Purchases ≠ Absorption of Market Duration

The Fed is purchasing short-term Treasury bills, not long-term coupon bonds. This does not remove the market's interest rate sensitivity (duration).

· Has Not Suppressed Long-Term Yields

Although short-term purchases may marginally reduce future long-term bond issuance, it does not help compress the term premium. Currently, about 84% of Treasury issuances are in short-term notes, so this policy does not substantially alter the duration structure investors face.

· Financial Conditions Are Not Broadly Loosened

These reserve management purchases aimed at stabilizing the repo market and bank liquidity will not systematically lower real interest rates, corporate borrowing costs, mortgage rates, or equity discount rates. Their impact is partial and functional, not a broad-based monetary easing.

Therefore, no, this is not QE. This is not financial repression. What needs to be clear is that the abbreviation does not matter; you can call it money printing if you like, but it does not deliberately suppress long-term yields by removing duration — which would push investors towards the riskier end of the curve.

That scenario has not materialized. The price action of BTC and the Nasdaq index since last Wednesday affirm this point.

What would change our view?

We believe BTC (as well as broader risk assets) will have their time in the sun. But that will come post-QE (or whatever the Fed terms the next phase of financial repression).

That moment will arrive when:

· The Fed artificially suppresses the long end of the yield curve (or signals to the market).

· Real Interest Rates Decrease (Due to Rising Inflation Expectations).

· Corporate Borrowing Costs Decline (Powering Tech Stocks/NASDAQ).

· Term Premium Compression (Long-Term Rates Decrease).

· Stock Discount Rates Decrease (Forcing Investors into Longer Duration Risk Assets).

· Mortgage Rates Decline (Driven by Long-End Rate Suppression).

At that point, investors will smell the scent of "Financial Repression" and adjust their portfolios. We are not yet in that environment, but we believe it is coming. While timing is always difficult, our baseline assumption is: volatility will significantly increase in the first quarter of next year.

This is what we see as the short-term landscape.

2. A More Macro View

The deeper issue is not the Fed's short-term policies but the global trade (currency) war and the tension it is creating at the core of the dollar system.

Why?

The U.S. is moving towards the next stage of its strategy: reshoring manufacturing, reshaping global trade balances, and competing in strategic industries like AI. This goal is in direct conflict with the role of the dollar as the world's reserve currency.

The reserve currency status can only be maintained as long as the U.S. continues to run a trade deficit. Under the current system, the dollar is sent overseas to purchase goods, which then flow back to the U.S. capital markets through treasuries and risk assets. This is the essence of the Triffin Dilemma.

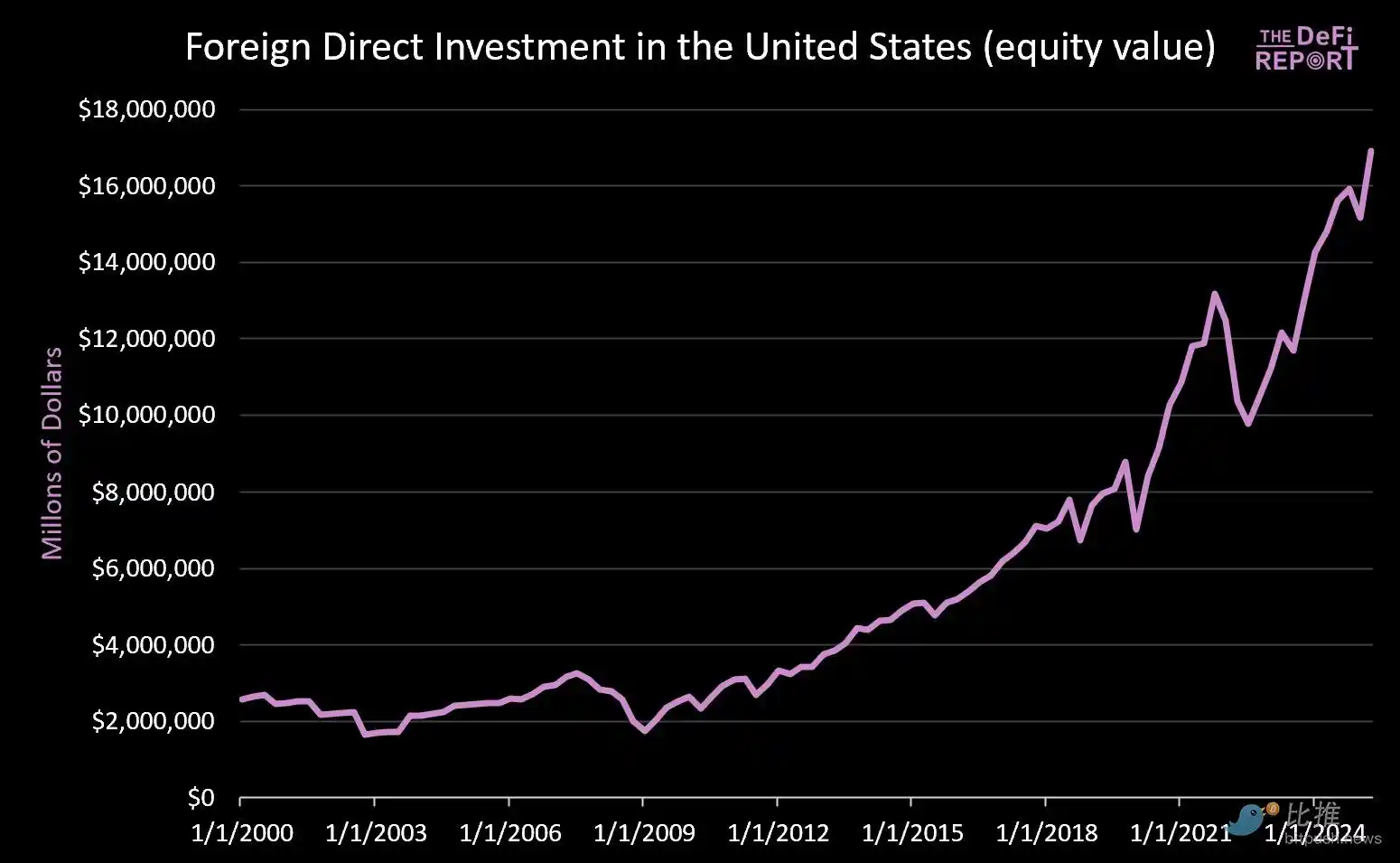

· Since January 1, 2000, the U.S. capital markets have received over $14 trillion (not counting the $9 trillion in bonds currently held by foreigners).

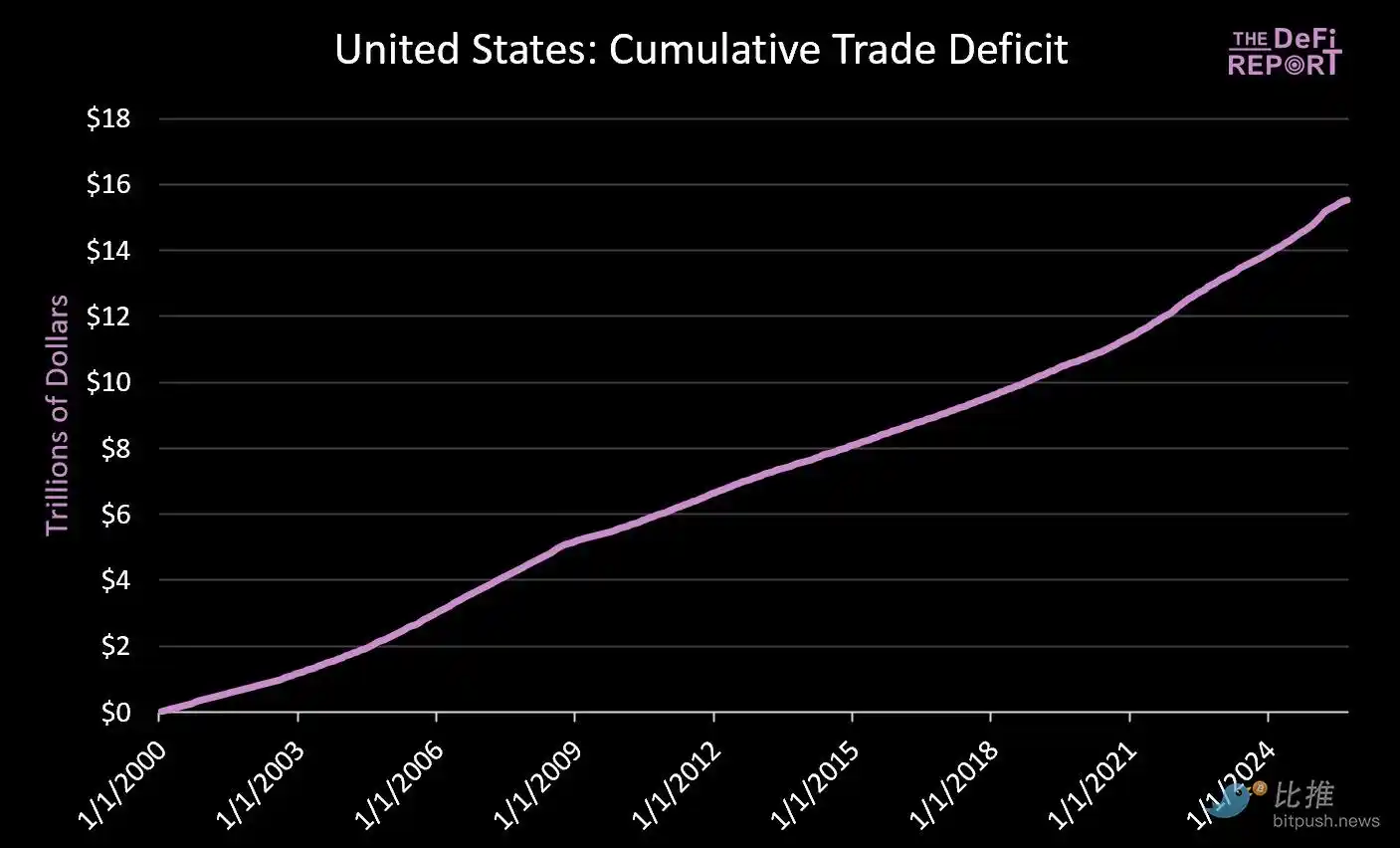

· At the same time, around $16 trillion has flowed offshore to pay for goods.

The effort to reduce the trade deficit will necessarily reduce the cyclical capital flowing back to the U.S. market. While Trump touts promises from Japan and other countries to "invest $550 billion in U.S. industry," what he fails to explain is that Japan's (and other countries') capital cannot simultaneously exist in manufacturing and capital markets.

We believe this tension will not be resolved smoothly. Instead, we expect increased volatility, asset repricing, and ultimately a currency adjustment (i.e., dollar devaluation and a shrinkage in the real value of U.S. Treasuries).

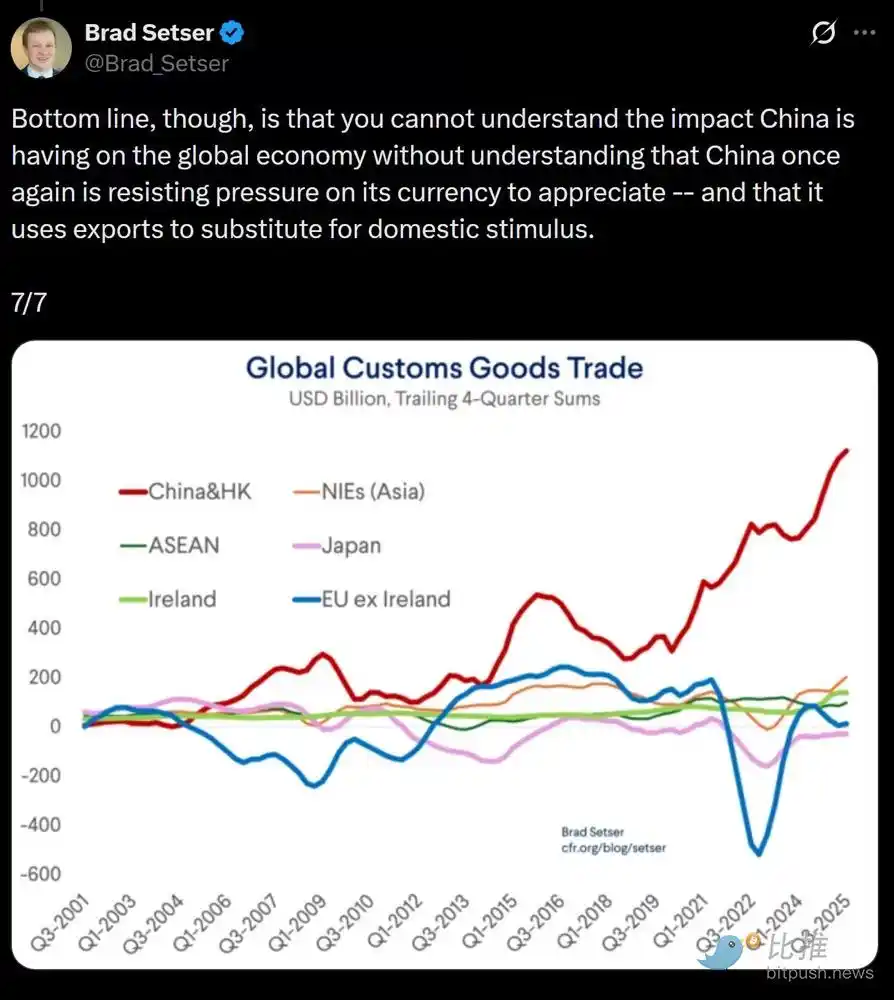

The core point is: China is artificially suppressing the value of the Renminbi (providing its export products with an artificial price advantage), while the U.S. dollar is artificially overvalued due to foreign capital inflows (resulting in relatively cheap import prices).

We believe that to address this structural imbalance, a mandatory devaluation of the U.S. dollar may be imminent. In our view, this is the only viable path to resolve the global trade imbalance.

In a new round of financial repression, the market will ultimately determine which assets or markets qualify as a "store of value."

The key question is, when all the dust settles, whether U.S. Treasury bonds can still play the role of a global reserve asset.

We believe that Bitcoin and other global, non-sovereign stores of value (such as gold) will play a far more significant role than they do now. The reason is that they are scarce and do not rely on any policy credit.

This is what we see as the "macro setup" being established.

You may also like

Former ByteDance employee's account: How I started with two Pinduoduo hard drives and made six times the profit with Seagate to achieve financial freedom?

Visa and Mastercard join 140 giants to launch a new stablecoin, but the impact on the market landscape may still be limited

WEEX Launches Depth Chart for Spot Trading

MiCA reshuffle begins, Binance temporarily bids farewell to the EU

Raising interest rates to protect STRC and selling coins to maintain credit, this time the strategy has chosen the two most expensive paths

Morning Report | Samsung announces a 265.5 trillion won investment plan, focusing on semiconductor and AI computing power data centers; Vitalik publishes an article detailing the entire technology tree behind the confusion protocol (iO) mainline

In the era of AI, what is left of Bitcoin?

NeoSoul announced plans to integrate with the OKX Agentic Wallet, promoting AI agents' participation in the on-chain economy

Why Is Bitcoin Lagging Stocks in 2026? AI Stocks, ETF Outflows, and the Nasdaq Rally Explained

What you bought on CEX is really not US stocks: Analyzing the 94% liquidation monopoly and the evaporation of equity under a five-layer pipeline

In such a crowded cross-border payment arena, where is the next stop for the future?

Why Is Bitcoin Down in 2026? What We Can Learn From 2022

The large models in the United States are moving towards closure in the name of security

From the white-haired stock god to the billionaire fund mogul, the smart people shorting Nvidia are all getting rich using the same framework

Morning Report | CoinEx becomes a key hub for Iran to evade sanctions, involving over $3.8 billion in funds; Kalshi seeks a new round of financing, with a valuation potentially rising to $40 billion

Global Launch: As predictions become the most scarce asset in the AI era, Manadia is defining the next generation of the value internet

Why do cryptocurrency projects always like to change their names?